Want to learn inventory cost accounting-cost of goods sold & sales of product income? Here is an article to aid you to find the details of all this. The inventory cost accounting and cost of goods sold feature is available while you set up QuickBooks Online Plus. What you paid for your item in your book is the value of an inventory. QB Online allows you to track 3 different types of items, inventory items, non-inventory items, and service. So, go through the article to collect all the information. For more info contact our Quickbooks ProAdvisor toll-free: +1-844-405-0904

Table of Contents

What is Inventory Cost Accounting

Inventory cost accounting includes incidental fees such as administration, storage, and market fluctuation. GAAP (Generally accepted accounting principles) uses standardized accounting rules to make sure that the companies do not overstate these costs.

It is part of the inventory control technique to ensure that the proper supply chain helps in reducing the total inventory costs and assists in determining the product for a company. All these factors help the company to find out how much margin should be assigned to each product or product type. The approaches for cost accounting are:

- Lean accounting

- Resource consumption

- Standard costing

- Marginal costing

- Throughput

- Resource consumption

Accounting Inventory Methods

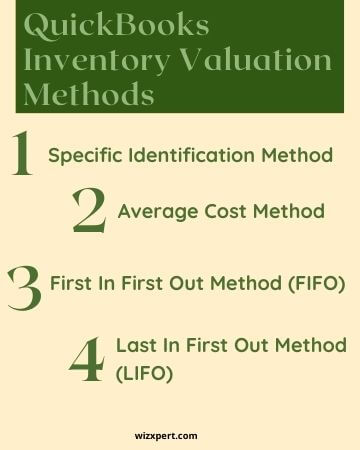

There are four methods of accounting inventory, check out the below points to know more in detail.

- Specific identification method: This method allows you to separately track the cost of every item in inventory and charge the particular cost of an item to the cost of goods sold when you sell the specific item to which that cost has been assigned. This method requires a large amount of data tracking, so it is only used for very high-cost, unique items, such as automobiles or works of art. It is not a viable method in most other situations. When you buy inventory from suppliers, the price changes over time, so you end up with a group of the same item in stock, but some units cost more than others. As you sell items from stock, you need to decide on a policy whether to charge the items sold that were likely bought first, or last purchased or the average of all items in stock on a cost basis. The policy of your choice will result in using either the first method (FIFO), the first last method (LIFO), or the weighted average method. The following bullet points illustrate every concept:

- First-in, first-out method: In the FIFO method, you are assuming that previously purchased items are also used or sold first, which also means that the items are still the newest ones in stock. This policy closely matches the actual movement of inventories in most companies and is therefore simply superior from a theoretical point of view. In a period of rising prices (which is the most frequent in most economies), assuming that the initial units purchased are used first, this also means that the least expensive units are sold at the cost of the goods previously sold. Is charged for. This means that the cost of goods sold decreases, leading to higher operating income, and more income tax to be paid. Furthermore, this means that there are fewer inventory layers than in the LIFO method (see next) because you will consistently use the oldest layers.

- Last in, first-out method. Under the LIFO method, you are assuming that the last purchased item has been sold before, which also means that the items are still the oldest in stock. This policy does not follow the natural flow of inventory in most companies; In fact, this method is restricted under international financial reporting standards. Assuming that the last units purchased have been used before, this also means that the cost of goods sold becomes higher, leading to lower operating income and lower-income taxes to pay. There are more inventory layers than the FIFO method, as the oldest layers may not be flushed for years.

- Weighted average method. Under the weighted average method, there is only one inventory layer, because the cost of any new inventory purchase is rolled into the cost of any existing inventory to obtain the new weighted average cost, which again after purchasing more inventory Is adjusted.

What is Sales of Product Income

The sales income account is an income/revenue account that records the sales of the products. And sometimes, this account is referred to as “Sales“ or “Sales of Product income”.

Difference Between Sales and Sales of Product Income Account

Sales of Product Income account is a default income account for the inventory items in QuickBooks accounting software while the Sales account is a default income account for non-inventory and services in QuickBooks.

What is the Cost of Goods Sold

The Cost of Goods Sold (COGS) is only affected when you sell any inventory items on invoices or sales receipts. After you sell an inventory item, and when you run a Transaction Journal Report for invoices/sales receipts and then view the Sales/Accounts Receivable transactions and you will be able to see the Inventory/COGS transactions which are credited into the Inventory asset account and debited into the COGS account.

You can adjust the charges of the bills, checks, and credit cards into the Inventory asset account and COGS account. But, you can only force these on the sale of inventory that you do not have. The amount on each side of the inventory/COGS transaction is equal to the Number of Items Sold x the Average Cost of the Item.

Cost of Goods Sold vs Inventory

The accountant records the difference in the cost of goods sold and inventory values as a part of their current assets. Therefore, the ending inventory balance is recorded as a current asset on the balance sheet. When the inventory increases, the asset on the balance sheet also increases. Also, when it decreases, the balance sheet’s current asset also decreases. The accountant records the change in inventory as a part of COGS.

Beginning Inventory + Net Purchases = Goods Available for Sale – Ending Inventory

The above COGS calculation is used by the accountant by adjusting some income statements.

Cost Flow Assumptions

If the Bookstore sells only one of the five books, which cost should Corner Shelf report as the expense of goods sold? Would it be a good idea for it to choose $85, $87, $89, $89, $90, or an average of the five amounts? A related inquiry is which cost should Corner Shelf report as stock on its balance sheet for the four books that have not been sold? Accounting rules enable the bookstore to move the expense from stock to the expense of products sold by using one of three cost flows:

- First In, First Out(FIFO)

- Last in, First Out(LIFO)

- Average

Note that these are the same cost flow assumption. This means that the order in which costs are removed from the inventory.

Different Reports that Ought to Keep Running on an Accrual Premise

Quantity on Hand (QOH), Cost of Goods Sold (COGS), and inventory Asset Account values might not be correctly indicated using a cash basis if the inventory is received and paid for in the future with a single or many payments.

The reports are:

- Inventory Valuation Summary

- Sales by service/product summary

- Sales by service/product detail

- Purchases by service/product detail

- Australia only – Stock report

The Bottom Line

Above, we have discussed various aspects of Inventory cost accounting like the cost of goods, effects of inventory tracking on the balance sheet, profit-loss statements, etc. And we also discussed the Sales of Product Income account and the difference between sales and sales of product income account.

To know more about inventory cost accounting you can contact our team of Intuit-certified QuickBooks ProAdvisor who possess great knowledge in the accounting and bookkeeping business. Call us at our 24/7 toll-free customer support number +1-844-405-0904.